Every item requires the decision to retain or remove. Consider these questions as you examine each item:

• When was the last time you used it?

• Do you believe you’ll use it again?

• Is there a sentimental reason to keep it?

You have four options for the things that you’re not going to keep. If you know someone who needs it or will appreciate it, you can give it to them. You can sell it in a garage sale or on Craig’s List. You can donate it to a charity and receive a tax deduction or you can discard it to the trash.

Start with your closet. If you haven’t worn something in five years, get rid of it. Then, go through the things again and if you haven’t worn it in two years, ask yourself the real probability that you’ll wear it again.

Another way to do it is to move it from your active closet to another closet. If a year goes by in the other closet, the next time you go through this exercise, those clothes are on their way out.

If the items taking up space are financial records and receipts, the solution may be to scan them and store them in the cloud. There are plenty of sites that will offer you several gigabytes of free space and it may cost as little as $10 a month for 100 GB at Dropbox to get the additional space you need. It will certainly be cheaper than the mini-storage building.

A ½% increase in interest rate may not sound like much but it is roughly equivalent to a 5% increase in price. It becomes obvious when you compare the payments.

A ½% increase in interest rate may not sound like much but it is roughly equivalent to a 5% increase in price. It becomes obvious when you compare the payments. Whether you continue to rent or decide to buy a home, according to recent

Whether you continue to rent or decide to buy a home, according to recent A certificate of deposit will generate a cash flow based on the interest rate that it pays which is the only way it generates a return for the investor.

A certificate of deposit will generate a cash flow based on the interest rate that it pays which is the only way it generates a return for the investor. “I’d wish I’d know that before I made a decision.” If you’ve ever regrettably said this to yourself, having a checklist might have prevented the issue in the first place. This list of questions can provide you with things to discuss when interviewing a moving company.

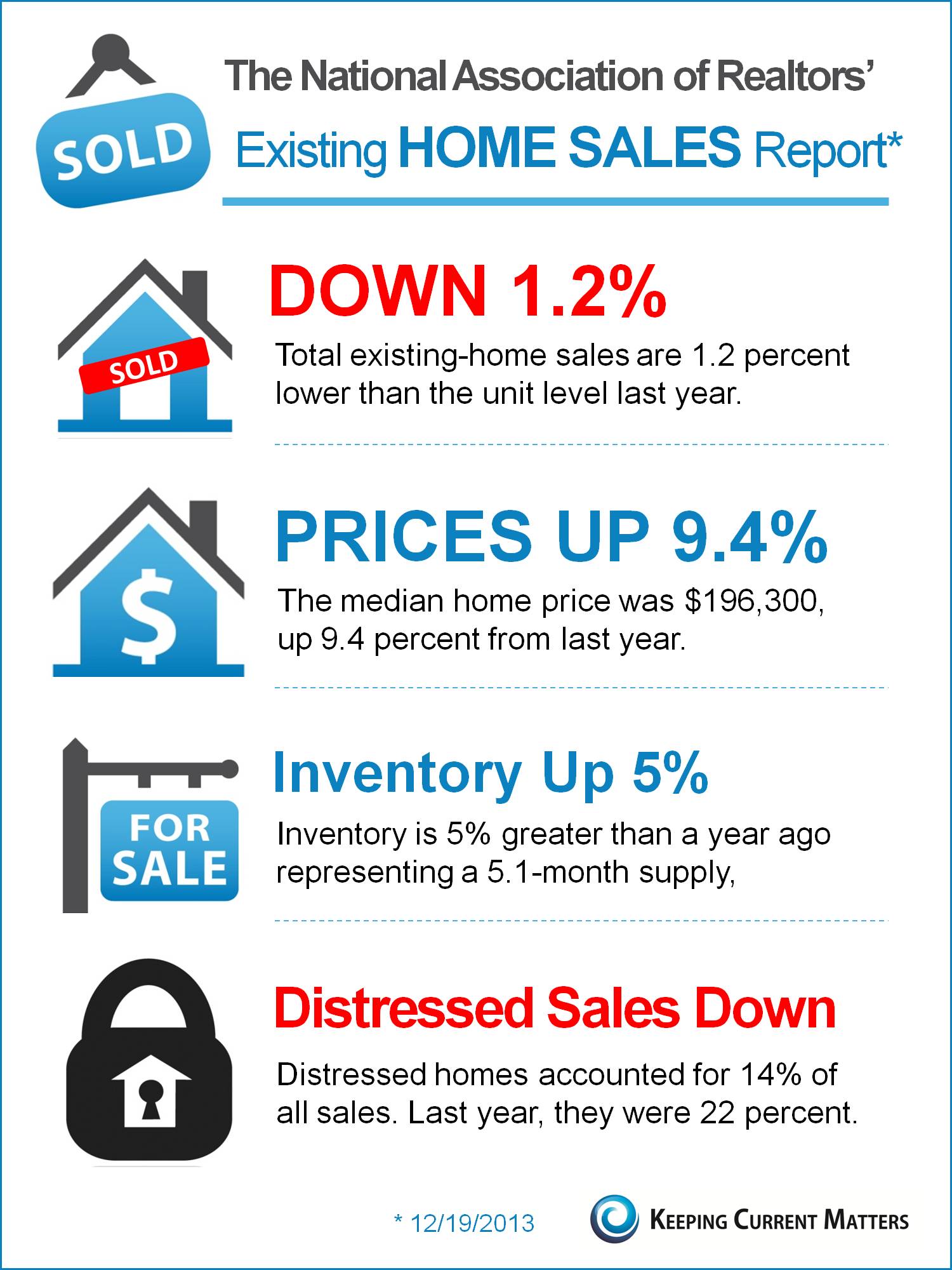

“I’d wish I’d know that before I made a decision.” If you’ve ever regrettably said this to yourself, having a checklist might have prevented the issue in the first place. This list of questions can provide you with things to discuss when interviewing a moving company. The two most frequently quoted constants in life are death and taxes. Two more things would-be homeowners can expect in the near future are increases in mortgage rates and housing prices.

The two most frequently quoted constants in life are death and taxes. Two more things would-be homeowners can expect in the near future are increases in mortgage rates and housing prices.

One of the most frequent calls from homeowners to their agents is about the listing’s inactivity due to the lack of showings. The homeowner commonly believes that the home is shown only when a buyer walks through the house with an agent.

One of the most frequent calls from homeowners to their agents is about the listing’s inactivity due to the lack of showings. The homeowner commonly believes that the home is shown only when a buyer walks through the house with an agent.

{kind=link}